The Rise of Affordable Housing Finance in India: Unlocking Dreams of Home-ownership🏡

#02 Highlights : This company targets a 35% AUM CAGR over the next 4-5 years, leveraging rapid branch expansion and OPEX optimization to boost profitability 🏛️

India Shelter Finance Corporation : A Growth Story Built on Solid Foundations 🏡

Disclosure : Invested & Biased

Industry Overview

The Indian housing finance market has been on a healthy growth trajectory, at a CAGR of ~13% (growth in loan outstanding) over FY19-FY23 to reach ₹29 lakh Cr. This growth is fueled by rising disposable incomes, increasing demand from Tier II and Tier III cities, attractive interest rates, and the government’s push for housing. The Affordable housing finance market is expected to continue growing in the coming years, with home loan outstanding projected to grow at 13-15% CAGR over FY23-FY26. Here are some key trends and statistics:

1️⃣ Market Size : India faces a significant housing shortage, estimated at 100 million units, with the majority of the need concentrated in the lower-income segment. Meeting this demand translates to a potential loan requirement of ₹58 lakh crore, a significant opportunity for the housing finance market.

2️⃣ Low Mortgage/GDP Ratio - Despite these positive trends, India's current mortgage/GDP ratio stands at a modest ~12.3% as of FY23, Other BRICS countries like China and South Africa have 28% and 21% respectively.

3️⃣ Government support: Government policies, such as enhanced interest subsidies under Pradhan Mantri Aavas Yojna (PMAY) and reforms in housing loan securitization under NHB, provide momentum for the affordable housing sector.

What is Affordable Housing Finance?

Affordable housing finance provides accessible and low-cost loans (Ticket size ₹10-₹15 lakh) to low & middle class peoples for purchasing, building, or renovating homes with Flexible Repayment options.

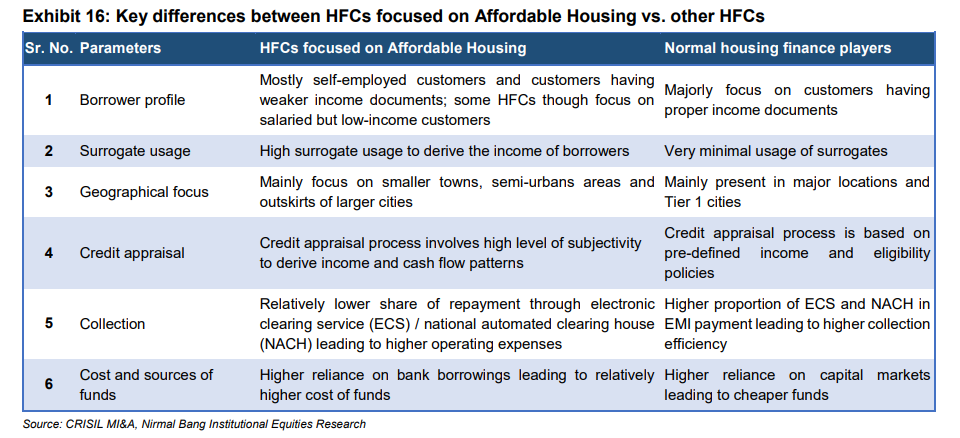

Affordable Housing Finance Companies (AHFCs) have carved out a strong niche in the market due to several factors:

1️⃣ Strong Focus on Target Segment: They cater specifically to low-income customers seeking housing loans below ₹15 lakh.

2️⃣ Deep Understanding of Micro-Markets: AHFCs focus on micro-markets allows them to gain in-depth knowledge of the local customer base and property values.

3️⃣ Direct Sales Teams: AHFCs rely heavily on their own direct sales teams to source home loans. This approach gives them more control over the customer relationship and loan origination process.

About the Company

Incorporated in 1998 , India Shelter specializes in providing affordable home loans & loans against property (LAP) targeting Tier 2 & 3 cities, focusing on first-time homeowners in Low Income (LIG) and Middle-Income Group (MIG) segments.

Having Recently crossed ₹7000 Crore AUM mark, the company has grown its AUM from ₹1,078 Cr to ₹7,039 Cr over the past five years, achieving a robust 35% CAGR.

Key features of India Shelter Finance's business model include :

1️⃣ Direct Sourcing : The company relies on a network of 260 branches across 15 states to source loans directly, eliminating the need for agents. This ensures better control over the loan origination process and helps maintain asset quality.

2️⃣ Tech-Enabled Processes : India shelter leverages technology extensively across its operations, from customer acquisition and credit underwriting to loan servicing and collections. This includes a digital loan approval process, mobility solutions, customer 360 view, artificial intelligence, and third-party integrations.

3️⃣In-house Underwriting : India shelter employs a team of experienced underwriting professionals who conduct rigorous due diligence on borrowers and property, ensuring a thorough assessment of credit worthiness and collateral value.

Asset Quality is all what matters

India shelter Finance corporation reported a 36% YoY increase in AUM to Rs. 7,039 crore, with strong growth in disbursements (26% YoY), PAT (62% YoY), stable ROA at 5.6%, and improved ROE to 14.8% with a 2.7x leverage while maintaining exceptional asset quality with GNPA and NNPA at just 1.2% & 0.9% respectively.

What’s Fueling this growth ?

Operational Efficiency : India shelter ‘s strong performance is driven by Robust underwriting, technology-driven operations, strong risk management , experienced management [Sudhin Choksey :Ex-MD Gruh Finance] and favorable industry dynamics supporting growth in affordable housing and mortgage penetration.

Branch-Level Performance Monitoring : This helps India Shelter Finance by identifying operational challenges, optimizing productivity, supporting strategic decisions, ensuring consistent customer experience, and maintaining strong risk management and compliance.

Future Outlook & Growth strategy

The Affordable housing finance sector in India remains largely underpenetrated, providing significant room for expansion.

1️⃣ Branch Expansion : India Shelter adds 40-42 branches annually, growing from a base of 220 branches last year to 260 branches this year and total 300+ branches planned next year. Company emphasized that new branches achieve breakeven within 8-9 months and contribute significantly to disbursement growth.

2️⃣ Operating Leverage: As the company scales up, its operating leverage should improve, leading to higher profitability. The OPEX/AUM ratio is is expected to reduce by 20-25 bps each year , improving from 4.5% to 4.25% by year-end.

3️⃣ Yield Sustenance: Company aims to maintain a consistent spread of 6%. They expect to sustain current yields due to their focus on Tier II and Tier III markets, where pricing tends to be higher. However, they acknowledged that they may pass on benefits to customers if the cost of funds decreases.

4️⃣ Management Guidance : ISFC aims for 30%-35% annual AUM growth for next 4-5 years , a consistent 6% spread, improved ROE to 16.5%-17% in 2-3 years, and maintains a credit cost guidance of 40-50 bps over the next two years, driven by increased profitability, operating Leverage & Enhanced Branch Productivity.

Peers Comparison : Asset Quality

Let’s Compare India shelter Finance with some of the listed Peers Home First Finance and Aavas Financiers based on various financial metrics including spread, ROA, Return on equity, operational Expenditure and other Asset quality.

Peers Comparison : Operational Metrics

This table highlights the operational and structural aspects of the three companies, giving a deeper insight into their business models.

Temporary Challenges in India shelter

1️⃣ Loan Against Property (LAP) Portfolio Performance: The LAP portfolio exhibits slightly higher delinquencies compared to the overall portfolio. They attributed this to seasonality factors and emphasized that the portfolio's relatively low LTV provides a buffer against potential losses

2️⃣ Increasing DPD 30+/GNPA: The recent rise in delinquencies, primarily in Madhya Pradesh, is attributed to internal manpower issues related to attrition and a lack of senior collection agents. The company has addressed this by strengthening its team in the affected areas.

Anti-Thesis For sector

Several challenges and risks faced by all Affordable housing finance companies:

Business Transfer (BT) Risk: As borrowers build a credit history, they may switch to banks offering lower interest rates. Mitigating this risk requires building strong customer relationships and offering value-added services.

Asset Quality Volatility: Long-term loans inherent to the housing finance industry make companies susceptible to asset quality fluctuations in economic downturns.

Competition from Banks: Banks with lower cost of funds may pose strong competition. While affordable housing finance companies may enjoy a niche market due to their specialized services and understanding of the segment, the threat of banks entering this market with aggressive lending practices remains.

Conclusion: Let the Numbers Guide You

From asset quality to operational efficiency, each company has unique strengths. If you prioritize industry-leading asset quality, Aavas Financiers might be your choice. For collection efficiency and Operating Leverage , India Shelter Finance shines. Meanwhile, Home First Finance offers strong scalability and growth potential.

Ultimately, the best investment depends on your risk tolerance, return expectations, and alignment with each company's strategic focus. Happy investing!

With Love & optimism❤️,

A View-Point from Investor’s Lens

Feel free to click the ❤️ button on this post If you find it useful, so more people can discover it on Substack . Tell me what do you think in comments ? Connect on X ID for faster updates & Research Reports are uploaded here .

See you next time, Happy investing!

Sources

1. Latest Financial metrics - Q2FY25 Investor presentation & Earnings Call

2. Affordable-Housing-Finance- by Nirmal Bang Institutional Equities Research

3. Research Report on India shelter Finance - ICICI securities

Great write up. Would be great if you add Aptus also in the comparison tables of operational and financial parameters.

Excellent 👌

Also shared about the company in X -

Result analysis -

https://x.com/DhawalDoshi5/status/1888191044531159389?t=1OQQQg-SuEV6mb0qLNJ5KA&s=19

Concall Analysis -

https://x.com/DhawalDoshi5/status/1890729018489704834?t=4UPgQKaUatuiGLCFIhy8WA&s=19