SG Mart : A Potential 5X-10X Bagger 🛠️

#01 Highlights: India’s first tech-enabled listed B2B marketplace for construction materials, Aiming for 50,000 crore in revenue with 1,500 crore in EBITDA 💼

Hii Folks, Publishing my First newsletter on Fundamental analysis of company. Do give your reviews in the comments

Deep Dive into SG Mart : The Game Changer in B2B Construction Materials 🏗️

Disclosure : Invested & Biased

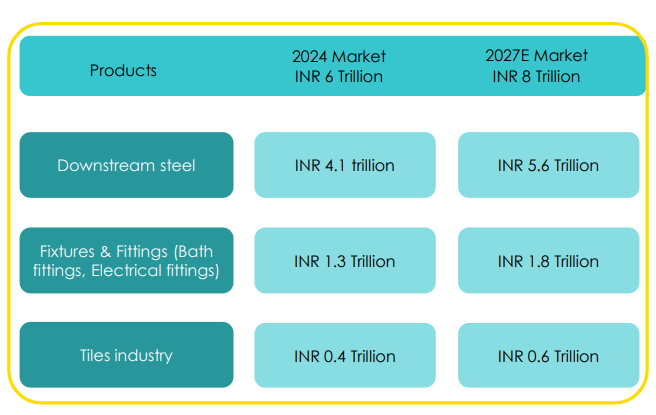

Industry Overview

India's B2B construction materials market, an industry projected to grow substantially in the coming years. This sector, valued at approximately INR 6 trillion in 2024, is expected to reach INR 8 trillion by 2027. This growth is driven by rapid urbanization, government infrastructure investments, and a shift towards digitalization in traditionally fragmented markets. As one of the few organized B2B marketplaces for construction materials, SG Mart is uniquely positioned to leverage these industry trends.

India's B2B marketplaces, which have experienced a 100-300% annual growth rate post-COVID, benefit from several supportive factors:

Increased digital adoption by MSMEs as they aim to improve operational efficiency.

Government Product Linked Incentive (PLI) schemes, Formalization due to GST and other regulatory measures.

Sector disruption by technology, with the penetration of B2B marketplaces at 1% today v. China / USA, where digital adoption is as high as 20%.

Addressable market - INR 6 Trillion B2B construction material Industry!

About the Company

SG Mart focuses on construction materials, especially steel. The company operates through three main revenue streams:

B2B Metal Trading: SG Mart buys in bulk from large producers and distributes to smaller dealers. Its primary products include HR coils, billets, and zinc.

Service Centers: These centers process raw steel for industries like automotive and construction.

B2C Distribution business : SG Mart also sells branded products like TMT rebars and other structural steel products.

SG Mart’s edge lies in its strong relationships with steel suppliers, including industry giants like JSW and Jindal Steel, and in its parent company’s (APL Apollo) established network.

Future Outlook

SG Mart has a clear growth roadmap, with targets and investments aimed at strengthening its position in the B2B construction materials market:

Service Center Expansion: SG Mart plans to expand its network of service centers to over 100 locations by 2030. Each service center requires an estimated INR 20-25 crore in gross block investment, covering land, building, and high-tech machinery, with an additional INR 10-15 crore in working capital. These centers are expected to generate approximately INR 350 crore in annual revenue per center at a 4-5% EBITDA margin. The centers will serve as both processing units and warehouses, reducing logistics costs and enabling faster delivery to key markets.

Revenue Growth Targets: SG Mart has set ambitious revenue goals, aiming for INR 7,000-8,000 crore in FY25, scaling up to INR 18,000-20,000 crore by FY27, and INR 50,000 crore by FY30. This growth will primarily be driven by the increased throughput from its service centers and expanded B2B and B2C distribution channels.

Product Diversification: While steel remains the core focus, SG Mart is gradually entering other construction material segments, including tiles and electrical fittings. This diversification allows the company to cater to a broader range of construction needs, further embedding itself as a one-stop solution for construction professionals.

Capital and Cash Flow Management: With INR 1,200 crore already raised from promoters and investors, SG Mart believes it has sufficient capital to support its growth objectives up to FY30 without the need for further equity funding. Its goal is to maintain a lean working capital cycle, with quick inventory churns and minimal receivables through a cash-and-carry model.

Peer Comparison: SG Mart’s growth potential and valuation opportunity

1. Of Business

Revenue Scale: OfBusiness has scaled aggressively with revenue reaching ₹20,000 crore in FY24, up from ₹15,000 crore in FY23 and ₹7,000 crore in FY22. This remarkable growth has been supported by strategic acquisitions and diversified expansion.

Valuation: Valued between $7-9 billion in the unlisted market, OfBusiness achieved a $5 billion valuation in its 2021 Series G funding round [by Tiger Global, SoftBank , Zodiac Capital ] when it raised $325 million.

Comparison with SG Mart: SG Mart’s FY24 revenue was ₹2,683 crore, positioning it at an earlier growth stage. While OfBusiness has already scaled significantly, SG Mart trades at a much lower valuation of ₹4,300 crore (approx. $500 million), indicating substantial room for appreciation as it scales its revenue and service infrastructure.

2. Infra Market

Revenue Growth: Infra Market has grown its revenue base from ₹350 crore in FY20 to an impressive ₹11,846 crore in FY23. This growth trajectory reflects rapid adoption and expansion within the construction and infrastructure segments.

Valuation: Currently valued at $2.6 billion, InfraMarket’s rise has been fueled by substantial funding rounds from prominent investors like Accel, Tiger Global.

Why SG Mart May Be Undervalued Compared to Peers ?🏅

Strategic Backing: SG Mart benefits from the Apollo Group’s industry relationships and funding strength, giving it a foundation for rapid scale.

Growth Potential: With an expanding service center network and ambitious revenue targets (₹7,000-8,000 crore in FY25 and ₹50,000 crore by FY30), SG Mart has a clear growth path ahead.

Valuation Opportunity: At a valuation of ₹4,300 crore, SG Mart trades at a fraction of OfBusiness and InfraMarket’s valuations. Given its established industry position and growth roadmap, this disparity suggests that SG Mart is well-positioned for re-rating as it continues to grow revenue and market presence.

This comparison highlights SG Mart as a potentially undervalued player in the B2B construction marketplace, with strong growth potential similar to its well-funded competitors.

Q1FY25 Financials

SG Mart’s recent financial performance highlights strong growth, reflecting its expanding footprint in the B2B construction materials market.

Here’s a breakdown of key financial metrics and trends:

Quarterly Revenue Growth: SG Mart reported INR 11,444 million in revenue for Q1 FY25. The company attributes this growth to rising demand, supported by an expanding customer and supplier base.

Profitability Metrics: In Q1 FY25, SG Mart’s EBITDA was INR 306 million (2.2% EBITDA margin), impacted by a one-time brand promotion expense of INR 59 million. Excluding this, EBITDA margins align with previous quarters’ 2.3% average. Net profit for the quarter was INR 263 million, driven in part by additional income from cash reserves invested in fixed deposits.

Return on Capital Employed (ROCE): The company’s ROCE stands at an impressive 51% annualized for Q1 FY25, reflecting efficient capital use across its low-margin, high-volume trading operations. SG Mart’s ability to maintain rapid inventory turnover, with a working capital cycle of just 5 days, underpins its high ROCE.

Investment Potential

Investment Thesis:

Solid Market Positioning: As one of the few organized players in a large and fragmented market, SG Mart has significant room for growth.

Strong Group Backing : The Apollo Group’s established reputation provides both financial stability and industry relationships.

Immense Growth Potential: With service centers and digital infrastructure expansion, SG Mart has a clear path to becoming a major player in B2B steel and construction materials.

Investment Anti-Thesis:

High Competition : Rising competition from established & new emerging players like of Business, infra market would mean deteriorating margins which essentially means that the triggers of growth are gone.

Execution Risks: Achieving nationwide service center penetration and handling the complexities of scaling B2C distribution may strain resources.

Dependence on Steel: Heavy reliance on steel trading could be a risk if demand for steel products decreases or if new entrants offer better pricing.

Conclusion

SG Mart stands at an exciting juncture in India’s rapidly growing B2B construction materials sector. With a clear growth roadmap, strong industry relationships, and the backing of the Apollo Group, SG Mart has positioned itself well for long-term growth. Investors may find SG Mart to be an appealing option in the B2B marketplace sector, although attention to margin stability and execution will be key to realizing its growth potential.

With optimism,

A View-Point from Investor’s Lens

See you next time, Happy investing!

Shankara buildings is also one of the peers. Here there is one more opportunity that company is planning for demerger. Previously APL Apollo was also one of the major investor which recently sold all its share in Shankara.

Revenue data is wrong.

Q1FY25 Qtrly revenue has degrown from 1277m to 1144m(Q4FY24).

Revenue for FY24 was 2683cr and not 3600cr.