Apollo Micro Systems Ltd : A Multibagger or Overhyped stock ?

#04 Highlights: The company is undertaking an ambitious 700% capacity expansion with two new facilities, including a 3,50,000 sq. ft. weapon integration unit, expected to go live by FY25.

Weapon Systems to MRO Services: Apollo’s Expanding Capabilities

Apollo Micro Systems operates in futuristic sectors like defense and aerospace, riding India’s modernization wave—and the market can’t seem to fund them fast enough.

In the last two years, they’ve raised over ₹700++ crore:

Nov 2022: ₹188 crore via convertible warrants.

FY24: ₹265 crore through preferential equity.

Jan 2025: ₹435 crore via equity and warrants.

Big mutual funds and HNIs [list here] are always onboard, but the company trades at lofty valuations while showing some red flags like increasing trade receivables, high finance costs & Negative Cash flow from operations.

Let’s break it down—hype or substance?

Industry Overview

India’s defense industry is on a fast growth track, driven by the government’s 'Make in India' push and a focus on modernizing its armed forces. Key drivers include government's focus on enhancing national security and reducing reliance on imports.

1️⃣ The Indian defense market is currently valued at around USD 90-100 billion and is experiencing rapid growth. With an anticipated annual growth rate of 13% from FY24 to FY30, it is set to become one of the fastest-growing defense sectors in the world.

2️⃣ India's defense budget has been steadily increasing, recently reaching ₹7,00,000 cr with policies encouraging import substitution with phased restrictions on 928 items.

India is becoming a major defense exporter, with ₹21,000 crore in exports in FY24. The private sector contributed 60%, highlighting strong growth potential.

About Apollo micro systems

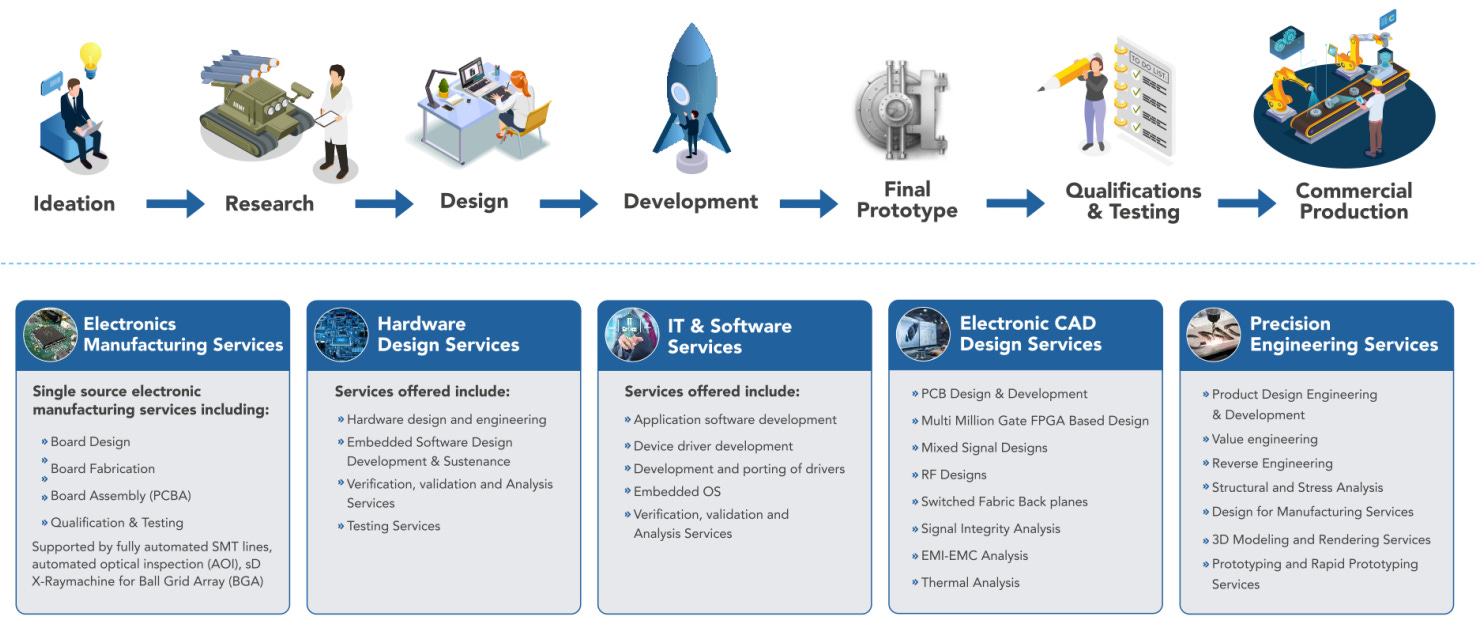

Apollo Micro Systems (AMS) business model revolves around being a one-stop shop for sophisticated electronic and electro-mechanical solutions, meeting the demanding needs of critical sectors like defense, aerospace, and industrial applications with solutions that work even in the toughest conditions.

1️⃣ Design & Manufacturing :

Custom Designs (Build-to-Spec): They create hardware and software solutions tailored to their clients' specific needs, from development to rigorous testing.

Precision Manufacturing (Build-to-Print): Using client-provided designs, AMS delivers high-quality, standards-compliant systems.

Electronic Manufacturing Services (EMS): From PCB fabrication to board assembly and testing, AMS leverages automated SMT lines and advanced inspection tools to deliver precision manufacturing.

2️⃣ Service offerings :

Defense: Rugged electronics for land, air, and sea missions.

Aerospace: Advanced on-board systems for aerospace projects.

Homeland Security: Embedded tech for monitoring and safety.

Manufacturing Services: From hardware design to IT integration, AMS supports a variety of industries.

Clientile : Ministry of Defence (MoD), Defence Public Sector Undertakings (DPSUs), DRDO and Private sector clients(Adani, L&T ) in the defence and aerospace domain.

Future Outlook

1️⃣ 700% Capacity Expansion: AMS's strategic investment in capacity expansion is crucial to meet the growing demand for its products and services.

IPiDS Facility : The newly inaugurated Integrated Plant for Ingenious Defense Systems (IPiDS) in Hyderabad, with a total investment of ₹210 crore, is dedicated to missile manufacturing and MRO (Maintenance, Repair, and Overhaul) services.

New Manufacturing Unit : The addition of new manufacturing units in Hyderabad, with a combined area of over 400,000 sq. ft, will significantly boost AMS's production capacity. This expansion is expected to be operational by 2025 and will enable AMS to take on larger and more complex projects.

2️⃣ Research and Development (R&D): A dedicated team of engineers focuses on developing cutting-edge embedded hardware and software solutions, investing 7-8% of revenue in R&D annually.

3️⃣ Collaboration with DRDO : AMS has a solid track record of delivering high-quality solutions and meeting client requirements, as evidenced by its long-standing relationships with DRDO and other key clients.

Management Commentary:

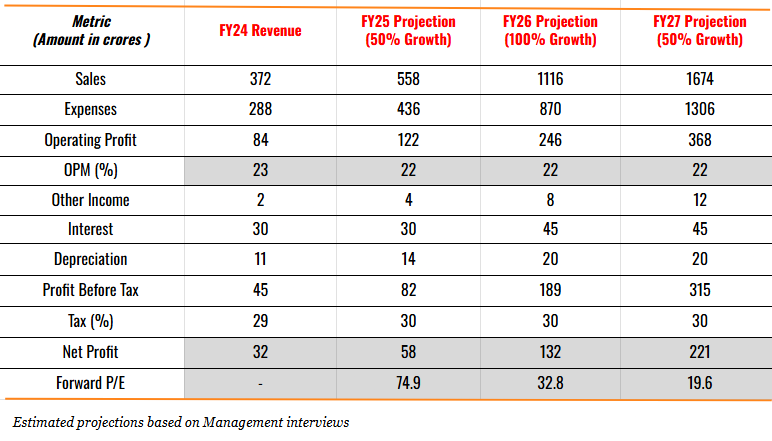

The management of AMS has expressed a highly optimistic outlook for the company's future performance, projecting strong revenue growth, sustained profitability, and expanding market share.

Revenue Guidance: Revenue growth of 20%-25% (Base case)in the coming years.

PAT and EBITDA Margin Guidance: EBITDA margins are projected to be maintained at a healthy 22%-24% due to expanding operations and operational efficiency.

As per Latest Bullish Guidance from Management

Anti thesis pointers

Liquidity and Cash Flow Risk: Negative CFO/EBITDA (107% ) for FY24, along with a cumulative OCF of just ₹11 crore against cumulative EBITDA of 282 Cr over the past 5 years, raises concerns about the company's ability to generate sufficient cash flow to cover operational needs despite positive EBITDA.

Working Capital and Financing Risk: High inventory levels (₹498 cr, 2x COGS) and extended trade receivables indicate potential liquidity issues, while the finance cost of ₹30 crore on average borrowings of ₹170 crore suggests significant reliance on external debt to fund operations.

Government Dependence: AMS's heavy reliance on government contracts can make it susceptible to changes in government policies, defence budgets, and procurement priorities.

Execution Risks: AMS's ambitious expansion plans come with inherent execution risks, including delays in project completion, cost overruns, and challenges in integrating new facilities.

Conclusion:

In conclusion, Apollo Micro Systems, with a market cap of ~₹4,000 crore, is a small-cap company with aggressive capex plans, reflecting a staggering 700% increase, signal its ambition to scale and solidify its position in high-growth segments like missile systems and MRO services.

Despite some risks—like increasing trade receivables, high finance costs—big investors, including mutual funds and HNIs, consistently show trust in the company. Their participation in multiple preferential issues underscores the growth potential and confidence Apollo inspires in institutional players.

Additionally, inventories are stretched, partly due to the company's involvement in around 80 programs, producing 200-350 subsystems annually. Receivables are also stretched, mainly due to the time required for product qualification and testing.

The big question remains: Can this small company execute flawlessly on its bold expansion plans and turn its high-risk, high-reward proposition into long-term success?

Ultimately, the best investment depends on your risk tolerance, return expectations, and alignment with each company's strategic focus. Happy investing!

With Love & optimism,

A View-Point from Investor’s Lens

If you found this article helpful, don’t forget to click the ❤️ button to help others discover it on Substack! I’d love to hear your thoughts in the comments—let’s keep the conversation going. For quicker updates, connect with me on X, ID and and Don’t forget to check out the referenced research reports here.

See you next time, Happy investing!

Sources

1. Latest Financial metrics - Q2FY25 Investor presentation

2. Management Inventories , Annual Presentations FY24

3. This newsletter is published based on data as per Jan 2025. Consider crosschecking.

Closed my Apollo Micro Systems (Small position) position at almost breakeven.

Part of Portfolio Restructuring /some Juicy SME investment opportunities .

Full analysis with key points previously shared.👇👇

Remember, it’s your journey—Trust your analysis and decisions! 💡

Note : I am not SEBI Registered. DYOR

Maybe mistaken. Appologies